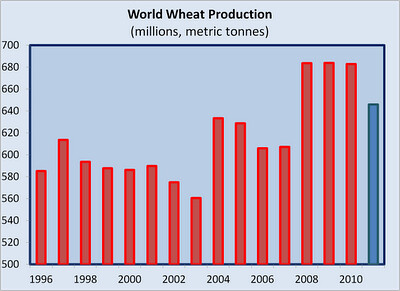

Unless a shortage is defined by a 0.1% decrease. Paul Krugman, with whom I often agree, has been crying hither and yon that rising food prices are a result of food shortages and not market speculation. This hasn't made much sense to me. First of all, we saw similar spikes in agriculture futures prices in 2006 that were clearly the result of financial speculation. First of all, as Alice Cook notes, we're producing historical high levels of wheat:

Curse those stupid fucking natural history facts! But there is a predicted decrease in supply of about five percent. Cook argues that this will lead to a speculative bubble:

Wheat prices are up about 50 percent in six months. The supply decline during that period was 0.1 percent. However, the anticipated decline in supply for this year is over 5 percent. That sounds a lot like speculation. Buy now on the expectation of higher prices in the future.Low interest rates facilitates speculation in wheat. Suppose a speculator can take out a loan at 1 percent, buy a few tonnes of wheat at $200, stash them away in a warehouse and sell them six months later at $325. Does that not sound like a familiar wheeze? Here is a clue; think houses, dot.com companies, and currency futures.

Meanwhile, the rest of the world pays more for their food. Moreover, there is a kicker. The greater the amount of inflation, the greater the incentive for commodity dealers to speculate. More speculation means more hoarding, which in turn, creates more inflation. There is only one thing that can stop this cycle - higher interest rates.

I disagree that higher interest rates are the solution. More accurately, we should have never undertaken quantitative easing. The problem is that, faced with two linked problems, idle capacity and idle workers, we are politically unable to engage in the obvious solution, which is deficit spending to prevent workers and industry from sitting idle. Instead, we are left with the option of flooding banks with quantitative easing. Oddly enough, banks, many of which still have questionable balance sheets, instead of loaning to businesses with inadequate demand (go figure), are shunting this flood of dollars into speculative markets, since, as Cook notes, that's where the (desperately needed) profits are.

As regular readers will know, I have no problems with deficit spending, but how one creates those deficits is really critical. The obvious way to solve the 'dual idleness problem' is through various employment programs--and it's not like our infrastructure isn't in need of a massive overhaul. The stupid way is quantitative easing: all this will do has done is fuel another speculative boom.

But, hell, maybe that's Plan B....

No, it's Plan A. Are you suggesting that America resort to something as gauche as actual productive activity? Why do you hate capitalism?

Buying in expectation of higher prices is also called "hedging." I'm not sure why higher prices now necessarily implies speculation.

Regarding wheat some people claim Chinese and other Asians start changing eating habits (westernization) moving from a rice-based cuisine to western ones and thus boosting request for wheat.

Also the summer fires in Russia and their blockage of wheat exports raised speculation over the wheat price

Steve: "Buying in expectation of higher prices is also called "hedging."

By those who do not understand the term. Consider the phrase "to hedge your bet". Buying in expectation of higher prices is a bet. To hedge that bet, you also do a comparable sale to lock in your profit or to reduce your risk.

After living in farm country all my life and covering ag as a journalist for 15 years I have to say I come down on Krugman's side on this one. I couldn't find a well done chart for wheat, but this chart for corn shows that while prices will be slightly higher than expected, they are not outrageous. I think part of the problem is also highlighted in the diagram by the cluster in the lower right part of the graph. It shows that prices were abnormally depressed from 1998-2007, making the the increases of the last few years seem even more extreme.

Min:

Actually, I understand the term quite well. Suppose I have or expect to have obligations to deliver wheat in the future. Suddenly I read that the Chinese wheat crop is expected to have a bad harvest. I start buying wheat options now. That's hedging, whether you agree or not. And it could lead to an increase in the price of wheat now.

The real point is that the evidence presented in this post for speculation is weak. If the demand for wheat is inelastic, then an expected future decrease in supply could cause a disproportionate increase in the price now. That's Econ 101.

I don't know if speculation is going on here or not, but I also don't expect an argument this weak to be endorsed by a scientist.

Min:

Actually, I understand the term quite well. Suppose I have or expect to have obligations to deliver wheat in the future. Suddenly I read that the Chinese wheat crop is expected to have a bad harvest. I start buying wheat options now. That's hedging, whether you agree or not. And it could lead to an increase in the price of wheat now.

The real point is that the evidence presented in this post for speculation is weak. If the demand for wheat is inelastic, then an expected future decrease in supply could cause a disproportionate increase in the price now. That's Econ 101.

I don't know if speculation is going on here or not, but I also don't expect an argument this weak to be endorsed by a scientist.

"If the demand for wheat is inelastic, then an expected future decrease in supply could cause a disproportionate increase in the price now."

True. And, given inelastic demand, even a small decrease in supply (when it comes) would cause soaring prices, even if speculation, hoarding, and futures trading were eliminated.

Steve: "Suppose I have or expect to have obligations to deliver wheat in the future. Suddenly I read that the Chinese wheat crop is expected to have a bad harvest. I start buying wheat options now. That's hedging, whether you agree or not."

But that's not what you said, Steve. :)

Min:

You're right. I should have been more precise in my original post. :)

The corresponding chart would have to be the silo capacity and utilization. They are are sacking wheat and storing it in warehouses, too damn expensive. If it is being stored it's in grain elevators. What is their volume on a historical basis. Many are in the hands of publicly traded companies or co-ops, their figures have to be available somewhere.

Alice Cook wrote this in one of her posts attributing the rise in food prices to speculation and dismissing climate change as a factor:

"I am fairly agnostic about whether the world is warming up. I just don't know. I am not a meteorologist. Nevertheless, I know one thing. This process, if true, will take many decades. Climate change won't burst upon us in six months and wreck our food supply."

Her arguments in favor of speculation are interesting but the brain-dead ignorance about climate change leads me to question her ability to analyze anything. I don't know what her economic credentials are but I do know Krugman's and all other things being equal I'll side with Krugman.

She's "not a meteorologist"? Meteorologists deal with weather, climate scientists study climate. Ms. Cook should learn the difference.

She proudly states "I know one thing" and then demonstrates that she doesn't.

Climate change is impacting the globe right here, right now. Hottest summer in Moscow ever. Thousand year floods in Tennessee. 20% of Pakistan under water. Brisbane flooded. Drought in China. Drought in Brazil.

You can't attribute any one event to global climate change but what you would expect from a warming planet is the increased incidence of extreme weather. Which is what we've been getting.

The expected impact of droughts on future harvests may be the sole reason for increased food prices or it may play a small role. The rise in food prices may be entirely driven by speculation. We'll know eventually. I only know that I'll look somewhere other than Alice Cook's blog for first-rate analysis.

I haven't analyzed this one too carefully, but when this came up about oil prices, it was pretty clear that most of the people arguing against Krugman didn't really have a good economic argument. You can come up with a lot of just-so stories about futures markets and how speculators or manipulators can magically make money by buying at one price and selling at another, but if you can't really draw the graphs in a way that makes sense, you're probably just blowing smoke.

Futures markets can affect spot prices by creating an incentive to hoard, which ends up being a reduction in supply on the spot market. That's the mechanism. So the simple question is, how much of the supply reduction is hoarding and how much is a "real" drop in supply due to other factors? Everybody wants to skip that piece of data and jump straight into the hand waving and chartology.

Of course, let's take the argument as it is: What Cook describes right now is futures markets working exactly as they should. Expected shortages in the future are causing "evil" speculators to store up commodities and smooth the supply over time. The add-on that this is causing a long-run feedback loop that can only be stopped by raising interest rates seems nothing short of insane--especially when one considers the fact that the current price shifts are, by Cook's own admission, driven by fundamentals. WTF?

This is food we're talking about. If this story is true and the shortage gets bad enough, spot prices will rise and cause an incentive to sell at the current spot price. That will slow the rise in futures prices and, since they're being held up by nothing other than self-fulfilling prophecy, pop the bubble. And a lot of speculators with grain silos hidden in the Bermuda Triangle or in underground FEMA camps will lose their shirts. Fiddling with interest rates is not necessary.

Well, yes...and no. It is primarily about speculation - and it is also about the fact that world food supplies are very tight. There's plenty of food, but biofuels, increased demand for meat and small decreases means that there's very little elasticity in the system, and that any sign of strain draws speculation, precisely because tight markets are desirable places to be. I agree that food prices are rising because of speculation, but it isn't necessary to stop there - food speculation is rising because of tight markets and an increasing number of car-people (consumers of grain as biofuels) and because of ecological pressures. It isn't just "turtles all the way down."

Sharon

Sharon, I would propose that food supplies are NOT tight, but that the money involved and the power (both from the money and from the fact that if your enemies don't eat, you won't have enemies for much longer) is immense.

See, for example, the CAP subsidies for European farmers that depress worldwide markets. The subsidy wasn't made for impoverishing third world farmers trying to sell their food (since they need money, not potatoes because Monsato et al won't accept barter in return for their agribusiness products), they were made to pay farmers who (especially in France) are a powerful political force. Removing CAP would help poverty and food security in the third world (since they woudln't have to sell so much edible food to get the money for their chemical help) but would have the French Government removed summarily.

Similarly, USA subsidies to their farming community (ensuring HFCS is used widely to the detriment of the health of USians as a whole, though since the farmers don't pay those costs, this externality is of no issue for them) ensure political power for the "Red States" with large farmer power blocks.

Then there are the internal demands. Warlords starving out (or being starved) opponents or supporters of the current regime, caste or similar societal impediments to freely move nutrition around to where it's needed.

There is also the need for the wealthy to accrue even more wealth. So when housing crashes, they move out (early) and put their money in the stock market. When that crashes, they move out (early) into land. If all that crashes, they move out (early) and put their money in food derivatives.

By the power of large volumes of money being applied and the complete disregard for any fundamental underpinning of worth and value, these movements of cash produce their own reason to occur. Where they move out, it crashes harder, where they move to, short term increases WILL be seen.

So though I think your conclusion broadly correct, the causation I believe quite different.

It isn't the multifarious uses of foodstuffs per se but the need of the rich to REMAIN rich and get even wealthier.

The actual food production is ample to feed the population, so the demand outstripping supply I think is not indicated by the data.

What about the other points Krugman made: increased meat consumption in China and the fact that unless someone is hoarding physical grain in warehouses that its not even clear how financial speculation could effect food prices.

@Wow: that post is logically incoherent. If food production is ample to feed the population, then why does it matter if CAP depresses the world food market? What was your point with that?

If farm subsidies make third world farmers less productive, then that results in less production. But thats not financial speculation, thats financial manipulation resulting in a real-world production drop that causes a legitimate price increase.

At the end of every future market and derivative there is a producer selling to a buyer. Without hoarding (which is possible maybe, but no one has claimed this is going on) its hard to see how these fancy financial footwork can really change that basic dynamic. The Great Recession should of taught us that.

Remember, Ian, stock market doesn't reflect actual demand any more. It's all about betting and siphoning off someone else's money into your account. Just look at the market cap for Cisco et al during the dot com boom for an obvious example.

Eating more meat in China will make a difference, but that hasn't been happening for long and those who can afford it in China aren't really a large number (compared to the size that "increased meat consumption in china" wishes to imply).

Wow:

This is kind of right and kind of wrong, but very illustrative. The stock market absolutely reflects actual demand--demand for the stock. Not demand for the products the company makes. Futures are the same.

As Ian is pointing out, supply and demand for food futures are not the same as supply and demand for food. If we jack up the demand for futures and drive the price of futures up, it does not necessarily affect the supply or demand of physical food. At the end of the futures contract, the same quantity of food still goes from somebody who has food to somebody who wants food, regardless of what the price of the contract did in the interim.

The only way for futures contracts to change the supply of actual food is to raise the future price of food high enough that people hoard it for sale later rather than selling it at the current market price. If no hoarding is happening and there's no decrease in supply, there's no problem. So where's the hoarding? In fact, is the incentive to hoard even large enough to be a problem yet?

This is similar (but not identical) to the oil situation. You can "hoard" oil by cutting production if you own oil fields. As far as I'm aware, you can only hoard grain by buying grain and putting it somewhere.

"As Ian is pointing out, supply and demand for food futures are not the same as supply and demand for food."

If that was what Ian was pointing out, then I agree. It just didn't seem to read that way.

"The only way for futures contracts to change the supply of actual food is to raise the future price of food high enough that people hoard it for sale later"

Or (for the market fundamentalists) by making it so profitable that people swap to produce it, displacing old use of land.

See the destruction of rainforests for an example.

That this is driven by short term greed and generally by people who do not reap the results of poor stewardship is merely the dirty underbelly of the free market that Ayn Randians and most prominent economists really loathe being talked about.

"@Wow: that post is logically incoherent. If food production is ample to feed the population, then why does it matter if CAP depresses the world food market?"

I notice I never answered that.

What happens is that the poor third world farmers have to sell more produce to get the US dollars that agribusiness want for their products. They won't accept bushels of grain for a bottle of insecticide.

This means less food left over to feed the country since that has to be sold on the export market to generate the cash.

That food is then wasted by the first world buyes, where, for example, entire herds of cows will be fed that grain then slaughtered so that

a) beef prices remain high

b) the farmers can claim compensation

Even if that food gets into the human food chain, we in the developed world throw away huge amounts of food.

No need to hoard the produce. We in the west will throw it in landfill.