Well, here it is:

Why am I showing you this? Mostly because its rather striking, partly because it forms part of the things Piketty got wrong thread, but mostly for the relevance to the "infinite growth on a finite planet" type argument. Many people will tell you that infinite "growth" on a finite planet is impossible, though they will usually be a touch vague about the meaning of the word "growth" (see Economics and Climatology? comments). Others will tell you that "economic growth" isn't necessarily resource constrained, and so infinite growth is perfectly possible.

Refs

* Piketty and the case for land capital - FT Alphaville.

* Land-shackled economies: The paradox of soil - the Economist: "Land, the centre of the pre-industrial economy, has returned as a constraint on growth".

* So why is it that everyone hates libertarians?

* Bjorn Lomborg demonstrates why universities should steer clear of him - Brian at Eli's.

* Murphy's Law? or, Follies of a Finite Physicist by Noah Smith. Taking Tom Murphy's "economist" apart.

* EconoTrolls: An Illustrated Bestiary

* Paul Krugman's Quite Right: Just Where Is All The Growth? - Timmy.

"Many people will tell you that infinite “growth” on a finite planet is impossible, though they will usually be a touch vague about the meaning of the word “growth” "

I find that people who tell you that infinite "growth" on a finite planet *is* possible get a touch vague about what they mean too (from memory there's usually some hand waving about qualitative growth).

I'm yet to read a satisfying answer to the issue that as long as generating a unit of GDP requires an energy input, surely as GDP tends to infinity so does energy consumption?

[Well, no. Suppose that the energy input per unit of GDP, at time t, is G/t. And the total GDP production is G*t. Then at any given time G*t is produced, and the energy input required is G. This doesn't obviously prove that can happen in the real world, it just demonstrates that your argument, as presented, is wrong -W]

Granted I'm sure that generating a unit of GDP could theoretically become extremely efficient and you could get an awful lot of growth for your energy input but an awful lot is not an infinite amount.

I feel that this graph demonstrates that an awful lot of growth is possible but it doesn't say anything about infinite growth to me (but I could be misinterpreting it).

OK fair enough. If the rate of improvement in energy intensity outstrips the rate of increase in growth then energy consumption wouldn't be a barrier to infinite growth. But that's a pretty heroic assumption :)

Huh, at first I thought that was a chart of topsoil loss.

But maybe it is, after all.

I believe a sensible interpretation of the graph is the slow growth of the land value of agricultural plots versus the skyrocketing valuations of urban land.

Jamie, if I buy a new widget (car, fan, washing machine) that uses less energy than what it replaces, the economy grows but the planet's net energy consumption does not.

The problem is more an illustration of the fact that economists, in general, have to be dragged kicking and screaming to apply their models to real world situations,

If 'growth' is reduced to an amorphous blob of completely interchangeable goods and services with the same bulk composition as today, and we insist on expressing growth in constant-percentage terms - then we have the 'infinite growth on finite planet' problem. If we get our hands dirty, start from a physical description of the economy and likely ways in which it will grow, then the problem goes away.

Jamie - you could imagine a situation where a constant population of perhaps 10 billion were all able to access heating, cooling, cooking, refrigeration and transport at 1st world levels or twice as much. Now - tell me how such a world would actually need more energy? They could create a basically unlimited amount of computer programs, art, personal services, etc without increasing energy use, so could have economic growth indefinitely. It's not like people are going to insist on heating their house to 40 degrees C instead of 25.

The answer to the infinite growth problem is that GDP is measuring "value" created. Not, absolutely not, resources consumed to create that value. As long as technology continues to advance (and a very wide meaning of "technology") then there's no obvious limit to what value can be added.

Yes, this is qualitative growth, as Herman Daly puts it, as opposed to quantitative. But the point does need to be made that traditional economics is already incorporating the two into that definition of growth, of GDP. Because it's measuring value created or added, not the volume of anything.

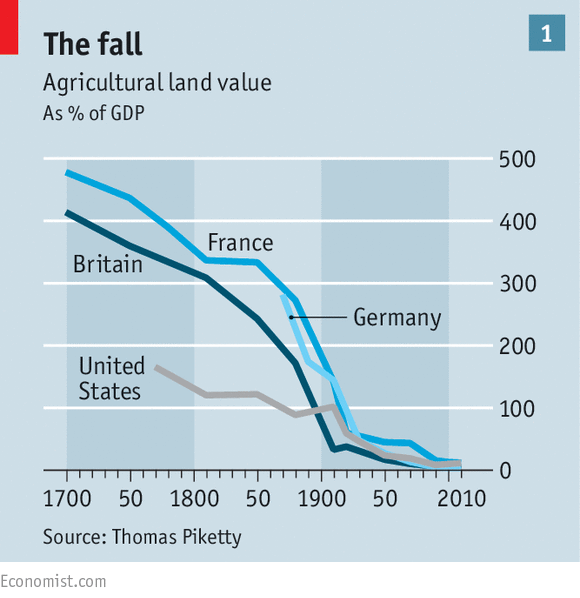

As to the land values, the other part of the same graph is most interesting. For while the value of ag land has fallen enormously, the value of residential land has risen, meaning that in 2015 total land values are about the same as they were pre-1900. Not exactly, but not far off.

The effects of the Town and Country planning acts, making planning permission an artificially scarce good.

Andrew (#6), can your hypothetical world of 10 billion first-world occupants ever exist? If the current first-world population is about 1 billion then the energy required for your 10 billion model would surely have fried us all to extinction. I suppose that would lead to constant energy demand!

Energy is needed to create computer programs, art, etc so energy demand will increase if you are producing an infinite number of them.

People might not want to heat their houses to 40 but they may/will need to keep them cool as the global temperatures continue to rise in your model world. Additional energy may also be required to keep the population at 10 billion, for climate mitigation/adaptation, more efficient food production, space exploration, etc. One of the things about first-world levels is that they are not constant but increase with time (aspirations). Can humankind exist in an egalitarian society or will there always be those striving for higher standards of living as we currently do?

Now you know why there are zombie movies.

Hoards of humanity escaping the urban areas as the food Nazis of the world say "No food for you".

Have absolutely no idea of what all the above graph means, and having an absolutely 111% "who gives a rats ass' ''tude, if I had to pick between being fed or feeding others, I'd go with feeding others, e. g. a farmer.

The Economist, it burns.

A major paradox of conservation economics is linked to the farmland fall ;

In most contemporyary markets, water is too cheap to conserve, and as a result , some nations lose more stored water by evaporation from their reservoirs than end users consume.

[water is too cheap to conserve - try telling that to John Fleck. Mind you, most countries (and the USA for sure) don't price their water sanely -W]

In praxis, "too cheap to conserve " means water prices per acre-foot ( or hectare/meter) far below the cost of an acre or hectare of any covering material that could be used to reduce its loss by evaporation,, down to and including oil slicks.

Even in the face of a drought and rationing, California farms continue to receive water for $30 to $50 an acre foot- a few dollars per 100 tonnes, allowing them to turn a profit exporting almonds and pistachios that cost up to ten gallons of water .each

> don’t price their water sanely

It's hard to compete with free.

Wasting the watersheds and collapsing the aquifers eventually eliminates that free problem but it's slow.

Once the free stuff isn't easy to get, you can put a price on it.

(I recall it's illegal to capture the rainwater off your roof for household use in Colorado, for example -- it all has to go from your rain barrels eventually into the water table -- not be diverted into the sewers and allowed to leave the state by going down the river.)

Ian Roberts -

My point is that the total imaginable energy use is large - although not large enough to directly fry the planet - but finite.

We can already see this in graphs of energy use per capita in countries that industrialize - it reaches an asymptotic point fairly quickly.

I would also say that simply expressing economic growth as a percentage value does not imply that it is exponential. Certainly, there is no reason to expect mature sections of the economy to grow exponentially or at all - I'm not eating 3% more bread a year, or using 3% more cars..

Is infinite growth possible in anything other than contrived and/or trivial cases? I doubt it.

First, we can rule out just about every scenario that doesn't cap population at some level. Second we can rule out every scenario that doesn't cap material growth; even a fixed population - say today's global population - can't grow infinitely in a material sense. Third, we can rule out just about every scenario that links energy to growth. While our energy supplies are large, they are not infinite. Even solar is a finite amount.

Basically that leaves us only with scenarios where we have a fixed population, with fixed material goods, and all 'growth' is qualitative. Or some space-faring/mining future where off-worlders send their newly discovered treasures back to Earth to fuel our infinite growth.

I think the idea that we can achieve infinite growth through qualitative changes is where the handwaving is most furious. This basically boils down to tomorrow's fad will be better than today's fad.

As for the space-faring scenario. I'm rooting for it, but I'm not particularly optimistic.

I nobody else is going to bring up Tom Murphy's argument against economic growth without resource usage growth I will have to do it myself.

http://physics.ucsd.edu/do-the-math/2012/04/economist-meets-physicist/

In the limiting case, everything necessary becomes free and so nobody is motivated to produce it, and we're all working very hard so we can afford to see the 5th sequel to the 12th remake of that awful Ultron movie whose special effects were so expensive that they are undetectable to the human eye, being on a scale our eyes can't resolve.

[I think that's flawed. The "main course" is about energy pricing and it doesn't really work. If you have a finite amount of energy then I agree it can't become arbitrarily cheap because someone will buy it all, but so what? And that important section concludes with the physicist merely asserting that econ needs to move to steady state; that's propaganda, not argument. And then in act 4 we have "Even if energy is fixed, and GDP is fixed..." which doesn't make sense. I think your physicist has misunderstood the meaning of GDP -W]

Like Murphy I find this scenario deeply implausible, but the immediate issue isn't infinite growth. The immediate issue is whether the west's "economy" can grow to a level to which everyone else can reasonably aspire. The implied dematerialization rate is enormous.

see http://initforthegold.blogspot.com/2009/05/cruel-hoax-growth-and-equity…

"Andrew (#6), can your hypothetical world of 10 billion first-world occupants ever exist? If the current first-world population is about 1 billion then the energy required for your 10 billion model would surely have fried us all to extinction. I suppose that would lead to constant energy demand!"

I hope so, or we're all rather wasting a lot of money on this climate change thing.

Seriously, go back to the SRES, the original economic predictions that underpin everything the IPCC did up to AR5. Have a look at the basic economic underpinnings of the families, A1, B1 etc. A1 assumes (assumes!) 7 billion people with a 5,550 trillion GDP. That's roughly your 10 billion first world people (roughly mind).

If they're powering that civilisation on coal (A1FI) then we've a serious climate change problem. If they're largely powering that society not on fossil fuels (A1T) then we've something between a very minor and a trivial problem with climate change.

And that is the only problem we have with that situation.

So, as I say, I hope we can have that all people are first world. Because we're already taking expensive action today on the basis that we will. Because we've predictied that it's likely that we will.

"I think the idea that we can achieve infinite growth through qualitative changes is where the handwaving is most furious. "

This isn't handwaving, it's definitional. Economic growth is an increase in value added. So, the limit to it is the value that can be added.

If you think that there will be a point where no more value can be added then fine, you think that growth is finite.

"If you think that there will be a point where no more value can be added then fine, you think that growth is finite."

But why that should be a problem is a bit of a mystery, Because the corollary to that statement is that us humans already have everything we could and do desire.

"The immediate issue is whether the west’s “economy” can grow to a level to which everyone else can reasonably aspire."

Super, go tell the IPCC all their models are wrong. Because they do assume this right at the start, that this is possible, indeed that it's likely that it will happen. That's why we're all working furiously on climate change of course, because that's a possible outcome of it happening.

[I think you blur the meaning of "IPCC" here, and "model". When you say "all their models are wrong" you're not talking about the models people associate with IPCC - the GCMs - at all -W]

> "But why that should be a problem is a bit of a mystery, Because the corollary to that statement is that us humans already have everything we could and do desire."

Does it follow? If we "reach a point where no more value can be added" due to us running out of a resource that could have created that growth, then this doesn't mean we "have everything we could and do desire". Maybe I am missing something.

"Does it follow? If we “reach a point where no more value can be added” due to us running out of a resource"

But that's not what my reference is to. Which is to not being able to figure out any more ways in which to add value: ie, technological advance comes to a halt.

I agree absolutely that we can't use more copper atoms than there are copper atoms on the planet. There are hard limits to greater resource use (they're vast, way out there, but they do exist, we have only 7,000 years left of mineral resources of phosphorous for example) and I'm entirely happy to state that there are.

Rather, my point is that adding value isn't constrained by resources. It's constrained by working out how to add value.

TW writes: "This isn’t handwaving, it’s definitional. Economic growth is an increase in value added. So, the limit to it is the value that can be added."

Of course it's handwaving. There's no way to actually show how this can be done - it's just assumed that we can continually add value to a product or service or replace it with a better product or service.

Worstall thinks of IPCC WG III as part of IPCC; hence IPCC WG III models are IPCC models.

You and I, of course, think of WG I as IPCC and the rest as baggage. Specifically, the CMIP models are the IPCC models and all other things are not the IPCC models.

But as far as the rest of the world is concerned TW is probably on stronger ground than we are. Unfortunately the reputation of IPCC rests to some extent on WG II and WG III.

"Worstall thinks of IPCC WG III as part of IPCC"

No, I'm saying that SRES is the set of economic models that all of IPCC, up to and including AR4 was based upon. That's where the emission pathways are derived from, after all. Yes, everyone's emissions pathways.

What will future emissions be? Depends: depends on the number of people, how rich they are and what energy generating technology they use. Exactly what the SRES explores. Which is why everyone, but everyone uses it.

Let's first short circuit the inevitable space cadet argument.

The arguments we are making here refer specifically to a planet. There are no limits to growth of a spacefaring civilization worth mentioning, as a whole. The limits in question regard the economics of a finite space with a finite set of physical resources. It seems very unlikely that a brisk trade will emerge between planets, so even if humanity succeeds in seeding the galaxy, the constraints, if they exist, on the individual settled planets will apply.

[Yes, stick to this planet. You're talking about Tom Murphy’s thing that you linked to? I've realised, thinking about it since I posted my last comment, that its far more badly flawed that I'd first realised. Its essentially one-sided: a wise clever physicist (who gets to write the minutes) talking to an economist who really hasn't thought through the issues at all (see the discussion on maximum usable energy, which the wise physicist explains to the silly thoughtless unprepared economist). So, right from that, we can see that its not the economist-side strongest arguments: the economist was clearly unprepared for the discussion. So, if you really want to see this discussed properly, you need to look elsewhere -W]

" So, if you really want to see this discussed properly, you need to look elsewhere -W]"

Well, yes, like here:

http://www.forbes.com/sites/timworstall/2012/04/12/economic-growth-will…

[Ah, thank you. I was going to ask -W]

I think Murphy was trying in good faith to explain as best as he could what the poor fellow he sandbagged was trying to say.

[He may have been. But its clear (see below; at least to me; I ask if you agree) that Tom M has misunderstood economics -W]

Perhaps this isn't the best possible counterargument and I do need to look elsewhere. I was hoping the elsewhere in question might be here.

[It is! Because Timmy is here -W]

On problem is that I don't think Murphy's argument exists outside blogs.

After all, if scientists thought this sort of stuff was worth publishing about I'd have scooped Weitzman by a decade on his fat tail stuff.

To summarize Murphy's claim

1) Assume physical resources are finite.

2) Assume economic activity grows without bound.

Then the limiting amount of physical resource per unit of economic activity goes within epsilon of zero.

[Yes. But there's a problem with all this "infinity" stuff. We who are mathematicians, and he who is a physicist, are happy talking in such terms, and thinking in such terms, but really... who can predict the future so far ahead? Its a nice game, but unlikely to be terribly real -W]

Then there is a confusion about how a market economy could function in such a condition/

A finite amount of physical resource is necessary, (and realistically far more important than all the bit-shuffling that we are calling "value" in this scenario.) This becomes a matter of trivial importance economically and the economy ignores it (per your graph we are headed that way).

So how does this work? How does the most essential thing get provided if in the limit nobody has any interest in providing it?

(In the real world, it appears that agriculture is increasingly done extractively as opposed to sustainably - a lot to discuss there but let's leave it aside.)

When last I brought this up to Tim, he raised the example of salt, which is vanishingly cheap and yet available. I've thought about this a bit.

I see a number of reasons that doesn't refute Tom. The most important of them is that the supply is not limited. The amount of salt available is not for practical purposes finite - it is not a serious resource constraint so that it becomes impossible to buy it all up.

[I don't think that works. Your puzzle just up above was How does the most essential thing get provided if in the limit nobody has any interest in providing it? The fact that there is loads of it lying around is clearly not the answer to such a puzzle. I can offer you another semi-answer to a different puzzle: the one Tom M raises: suppose energy use is limited by physics, and so the economic cost of energy declines as a proportion of activity, so that someone could buy it all... ZOMG contradiction. But consider salt: the annual economic salt activity is probably low enough that Bill Gates could buy it all. But (a) why would he bother, and (b) if he tried to corner the market, the price would go up -W]

So the question for the economist is whether there is a way for stuff which is in limited supply and very high inelastic demand to be a vanishingly small proportion of the economy.

Murphy hasn't proven the contrary, but it certainly goes against what I know about how markets work.

The key to Tom's argument then is that in the limit of infinite growth, real supply limited resources must cost zero.

If that cannot happen, there is a limit to dematerialization.

Whether that bites soon enough to matter for our present predicament is an argument that one could still have in the light of Tom's argument. Let's do, by all means.

But if there's a way out of this problem in the long run, it is very hard for me to imagine it.

One commenter said to me "I do want to be clear I think we are better served IF we can change the goal completely. Happiness, self-fulfillment, and having basic needs met are worthy goals that don't doom us to extinction or collapse. Seeking continually growing material wealth or economic growth doom us to an unhappy future at best. I like your notion that perhaps we can all be delusionally happy if we are simply given more Monopoly play money and it has no connection to more resource depletion or environmental degradation! You may be onto something."

http://initforthegold.blogspot.com/2009/04/malthusian-in-theory-but-not…

What I've seen since is that it isn't just a peculiar notion of my own - it seems to already be the conventional wisdom!

At best this seems to be a description of the future you are proposing; as I looked further into it I determined that the required rate of converting the economy from real money to play money is probably too rapid to work.

[Don't mistake me; I'm not proposing anything; I'm just saying this is how the economic meanings of words goes -W]

A possible compromise I could imagine is socializing everything substantive and "growing" an economy of ideas in parallel. That could work. I am guessing this isn't what you all are after, though. One wonders if there aren't limits to growth in that world as well.

The real handwavy part is "what is the thing that is growing?"

We crossed in the mail. I just read the Forbes piece and it seemed like conventional wisdom. I didn't think it was responsive to the main argument at all.

Let's rephrase the claim - not that growth is impossible, but that growth is bounded.

One can continue approaching a bound without reaching it. (100 - (exp(-t))) approaches 100 from below without ever reaching it at t goes to infinity. But that's more like a steady state economy than a growth economy.

[I think you're still missing the main point that Timmy is making. Which is: that the thing economists call "economic growth" - crudely, as GDP growth if you like - isn't tied to resources, really. It appears to me that this is so antithetical to what you think growth ought to be that you can't see it. Or am I wrong?

Also, notice that Tom M has misunderstood GDP. And Timmy's Forbes piece points this out. Do you accept that Tom M has clearly misunderstood GDP? There's not much point going on if we can't agree on that point -W]

"[Yes. But there’s a problem with all this “infinity” stuff. We who are mathematicians, and he who is a physicist, are happy talking in such terms, and thinking in such terms, but really… who can predict the future so far ahead? Its a nice game, but unlikely to be terribly real -W]"

Stipulated. It's an open question so far in the conversation whether this is of immediate concern on realistic policy horizons. (I think it is.) But first we have to agree, as you say, on whether there is a real problem at all.

My point is exactly that it is NOT possible for a billionaire to corner the salt market. (Your government tried that in India once by fiat.) The problem with controlling the salt market is that there is plenty of salt.

The market-cornering thing is just one aspect of the problems that arise when the things people want most (food) have a cost of epsilon.

Look, prices are set by an equilibrium of supply and demand. If everybody has more "money" then they are willing to spend more on essentials, say, food. So the proportion of real goods in limited supply in the economy cannot go to within epsilon of zero.

This does not apply to salt because the supply is not in principle limited.

To my understanding mainstream economics has no real theory for such limitations and so is very eager to handwave them away.

"[the thing economists call “economic growth” – crudely, as GDP growth if you like – isn’t tied to resources, really. It appears to me that this is so antithetical to what you think growth ought to be that you can’t see it. ]"

I think we have on the table an argument that it is indeed tied to resources. That's exactly what we're discussing if we're discussing Murphy's piece.

It's not what I'd "like" in any ordinary sense. I'd much prefer the contrary, as it would make our immediate policy problems much easier if we didn't have to threaten the assumptions of the financial world. I started out trying to convince myself that this was possible, and I convinced myself instead that it was not. If you can unconvince me it would please me.

(Just as it would please me if you could unconvince me that CO2 is a problem and that policy response to that problem is woefully late...)

> [ Do you accept that Tom M has clearly misunderstood GDP? There’s not much point going on if we can’t agree on that point -W]

That seems a bit abrupt. No I think it's less accurate to say he misunderstands it than to say he framed his position hastily and had to retreat a bit.

[I don't know what you mean by "had to retreat a bit". I've only read that one piece of his; that's the one you pointed me at. If he retreated in another piece, you'll need to tell me where.

The problem is clearly seen in But he had to ultimately admit to a floor on energy price and therefore an end to traditional growth in GDP—against a backdrop fixed energy. Which to me is WTF? Why does a floor on an energy price, and fixed energy, imply and end to GDP growth? That seems completely wrong to me; it implies an misunderstanding of GDP. Do you think its correct? -W]

Insofar as "money" is well-defined, GDP is well-defined. It isn't exactly rocket science. Inflation-adjusted GDP is a bit stickier, and we need that to talk about long term issues, but I don't see that Tim has made a case that misdefining GDP is a fundamental flaw in Murphy's argument.)

As I said, yes he did have to retreat a bit. That retreat is why I have changed the thesis from a vague claim that "endless growth is impossible" to a more precise one that "growth is bounded".

The point is not that dematerialization is impossible. .

Obviously it is possible, and your chart does in fact illustrate that point. The point is that the illustrated trend (which really hides several things under one rubric - expanding industry, expanding non-material production, increasing agricultural productivity, offshoring of food production) probably has to stop somewhere at least on a global measure.

It helps, but can it help enough? Murphy's point is that it cannot help enough indefinitely.

I believe that when we look at extant carbon footprints, aspirations for continued growth in the developed countries, aspirations for development in the rest of the world, and any reasonably equitable international order, it turns out we are asking far too much of this process of decoupling the economy from resources to be realistic.

If anyone decides to take this problem seriously, presumably there is a name for the quantity of interest. Call it resource intensity. I believe that the scenarios which economists favor implicitly carry a tenfold to fiftyfold decrease in resource intensity in this century.

It's another instance of the sort of crypto-over-optimism thinking that David Roberts alludes in his recent notorious essay.

http://www.vox.com/2015/5/15/8612113/truth-climate-change

[DR's piece quotes the World Bank report as saying according to a 2012 World Bank report, "extreme heat-waves, declining global food stocks, loss of ecosystems and biodiversity, and life-threatening sea level rise". But it doesn't actually say this. Its the familiar confusion between food production, including all factors, and the effects of climate change considered in isolation. As to the rest: And so, awful shit it is. Nobody wants to say that. Why not? My reason is that I'm still not convinced that "awful shit" is a good description. As I said about the WB report before -W]

[I shall risk adding another follow-up, that you might not see. Another point is: this isn't as important as you might think. "GDP growth" isn't necessarily what you care about. You're not obliged to. Many people have said its a poor measure of "true welfare" whatever that might be -W]

Would the layman be wrong if he took away from this discussion a need to classify growth in the three types mentioned? I see 1.growth in knowledge of extracting value more efficiently. 2. growth in energy supply to manipulate resources 3. More resources extracted.

Any combination of these would lead to growth, correct? With none, growth is not possible. Is that also correct?

"I see 1.growth in knowledge of extracting value more efficiently. 2. growth in energy supply to manipulate resources 3. More resources extracted.

Any combination of these would lead to growth, correct? With none, growth is not possible. Is that also correct?"

I wouldn't say extracting value but adding value. Because value is not something inherent in anything, it's an attribute which we humans apply. it comes from our views.

But other than that, pretty much. My point being that in a steady state economy (where 2 and 3 are bounded) we still have 1 to produce growth. And if 1 is also bounded, then sure, we can't have any more growth.

Re the David Roberts piece:

"The red line is the status quo — a projection of where emissions will go if no new substantial policy is passed to restrain greenhouse gas emissions."

It isn't RCP 8.5 is a business as usual projection. As are all RCPs business as usual projections. Just like the earlier SRES, all are possible mixtures of socio-economic, demographic, energy generation and radiative forcing models. None of them assume or require substantial new policy. That's how the models are designed in fact. To sow what might happen without mitigation policies.

Tim,

As are all RCPs business as usual projections. Just like the earlier SRES, all are possible mixtures of socio-economic, demographic, energy generation and radiative forcing models.

I don't think the latter point is correct, well unless you mean something different to what it seems. The underlying radiative forcing models are the same for all the scenarions (i.e., the response to a change in radiative forcing is the same for all the RCPs for the same underlying model).

None of them assume or require substantial new policy. That’s how the models are designed in fact. To sow what might happen without mitigation policies.

I realise that none of the RCP assume anything about policy (I think), but I fail to see how we can achieve some of the possible pathways without substantial changes in policy. Even imposing a carbon tax, would - I would argue - require substantial changes in policy. So, I don't think it is correct to describe them all as models that show what might happen without mitigation policies, unless you really think that we can follow something like RCP2.6 or RCP4.5 without any mitigation policies.

Presumably, when you argue that all RCPs are business as usual scenarios, you mean that they're all technically possible future scenarios and hence, the one we follow will be the "business as usual" pathway. That is not what other people mean when they use "business as usual".

"unless you really think that we can follow something like RCP2.6 or RCP4.5 without any mitigation policies."

4.5 is, roughly enough, SRES B1. Which specifically did not require mitigation policies.

"Presumably, when you argue that all RCPs are business as usual scenarios, you mean that they’re all technically possible future scenarios and hence, the one we follow will be the “business as usual” pathway."

No, I mean that when someone says "bau" they always, but always, mean RCP8.5. And that's simply not true. While I might change a little bit for 2.6, 4.5 and 6 can be reached, they say they can be reached, without mitigation policies.

"That is not what other people mean when they use “business as usual”."

Yes, that's what I'm complaining about.

Just to rub this in: 8.5 assumes 12 billion people, with coal making 50% of energy (a 10x increase in current consumption). In what manner is this business as usual?

Tim,

4.5 is, roughly enough, SRES B1. Which specifically did not require mitigation policies.

Well, it would be interesting to see some evidence for this. Also, I assume you mean that it was assumed to not require mitigation policies, rather than it definitively being achievable without mitigation policies.

While I might change a little bit for 2.6, 4.5 and 6 can be reached, they say they can be reached, without mitigation policies.

You seem to be focusing on the word "policies" rather than on the word "mitigation". The lower emission pathways require a bigger role for alternatives, than the higher emission pathways. Most regard this as a form of mitigation (as opposed to adaptation). Whether you want to call how we decide to do this a "policy" or simply some alternative way of achieving this would seem to be a secondary issue (we won't follow one of these pathways purely by chance).

Yes, that’s what I’m complaining about.

Except, the exert from Roberts that you quote didn't use it.

Just to rub this in: 8.5 assumes 12 billion people, with coal making 50% of energy (a 10x increase in current consumption). In what manner is this business as usual?

I've no idea. I wasn't defending it. I was simply pointing out that many who use BAU mean a scenario in which fossil fuels dominate and we continue to increase our emissions along an RCP8.5 pathway - or close to an RCP8.5 pathway. You may not like the terminology (I might even agree) but it would seem better to criticise what they were trying to say, rather than what you claim they're saying by choosing to define the terminology differently to what was intended.

However, I still think your claim that none of the RCPs require substantial new policies is not correct. Or, rather, that it's very hard to see how we can follow some of those pathways without substantial new policies. It might be theoretically possible, but I find it difficult to believe that it is actually possible.

"You seem to be focusing on the word “policies” rather than on the word “mitigation”. The lower emission pathways require a bigger role for alternatives, than the higher emission pathways. Most regard this as a form of mitigation (as opposed to adaptation)."

Mitigation has a specific and exact meaning here. It is "changes in regulatory or legislative policy to reduce emissions".

So, for example, a carbon tax, cap and trade, these are mitigation policies.

Something that happens without a specific regulatory or legislative change is not a mitigation policy. It is, instead, one of the possible business as usual scenarios.

So, imagine, solar power really does become, everywhere, cheaper than coal fired from the grid. Obviously, large numbers of people will install solar.

If solar has become cheaper as a result of public policy (feed in tariffs etc) then that's a mitigation policy. If solar has become cheaper simply because the market has become better at making solar panels then that is not a mitigation policy, that is business as usual.

The difference, mitigation or bau is whether or not there is intervention, not whether or not there is change.

I agree entirely and absolutely that change is necessary. The argument, from my point of vierw, is how we get it. And I'm a great deal less convinced of the necessity for intervention, ir that mitigation.

Please do note, these are not my definitions. They're the ones baked in at the beginning of the IPCC process. Thus we all should be using them when discussing the IPCC outputs.

Does the world need to change? Sure, yes. Without public policy changes (ie, intervention or mitigation) is RCP 8.5 the inevitable outcome? Nope: 6.0 and 4.5 are entirely possible as baus, without intervention or mitigation.

This was all much clearer with the earlier SRES where this was specifically and openly laid out. All 40 scenarios were business as usual. Mitigation was whatever we did on top of them.

Tim,

Mitigation has a specific and exact meaning here. It is “changes in regulatory or legislative policy to reduce emissions”.

Can you provide a link, well unless you mean "mitigation policies" as opposed to "mitigation", in which case I agree. I've certainly seen the term "mitigation" being used in the context of reducing our emissions without it being explicitly tied to a policy.

So, for example, a carbon tax, cap and trade, these are mitigation policies.

Yes, in fact I think I gave a carbon tax as an example myself.

I agree entirely and absolutely that change is necessary. The argument, from my point of vierw, is how we get it. And I’m a great deal less convinced of the necessity for intervention, ir that mitigation.

Well, if you include that we don't even need something like a carbon tax, then I would disagree.

This was all much clearer with the earlier SRES where this was specifically and openly laid out. All 40 scenarios were business as usual. Mitigation was whatever we did on top of them.

Again, it would be nice if you could provide some kind of link.

Opening lines of SRES report:

http://www.ipcc.ch/ipccreports/sres/emission/index.php?idp=24

"The SRES writing team formulated a set of emissions scenarios. These scenarios cover a wide range of the main driving forces of future emissions, from demographic to technological and economic developments. The scenarios encompass different future developments that might influence greenhouse gas (GHG) sources and sinks, such as alternative structures of energy systems and land-use changes. As required by the terms of reference however, none of the scenarios in the set includes any future policies that explicitly address additional climate change initiatives 1 although all necessarily encompass various assumed future policies of other types that may indirectly influence GHGs sources and sinks."

As to why, a couple of paras down:

"Possible climate changes together with the major driving forces of future emissions, such as demographic patterns, economic development and environmental conditions, provide the basis for the assessment of vulnerability, possible adverse impacts and adaptation strategies and policies to climate change. The major driving forces of future emissions also provide the basis for the assessment of possible mitigation strategies and policies designed to avoid climate change."

Obviously: we can only figure out the costs and benefits of a mitigation strategy if we've already laid out what will happen without one. The scenarios are without, so that we have that base against which to measure a mitigation policy or strategy.

Thus, A1T (not considered in the RCP) or B1 (roughly, RCP4.5, emissions from A1T are similar but richer world, less emitting technology as the pathway to it)) could happen without any mitigation policies at all.

The importance of this is that if that is indeed true then the mitigation policies we would need to get to RCP 2.6, just as an example, would be fairly trivial.

"if you include that we don’t even need something like a carbon tax, then I would disagree. "

My standard position is that every economist who studies this says let's have a carbon tax. And on insurance grounds at the very least, yeah, OK.

My own belief, not something I would want to have to prove, and not something that should perhaps inform public policy either, is that we've already done enough. From that SRES it's obvious that if we can decarbonise, to a great extent, the energy generation systems then we're done. That's roughly A1T. And if you look at the detailed estimates of energy production that make that up I'd say we're ahead of schedule there. Because it's not deployment of, say, solar that matters, it's getting it cheap enough that people will naturally, preferentially, install it. And we're just about there, aren't we?

Problem pretty much solved.

In my more cynical moments I start to think that those screaming about how we've got to do it all now, Now, NOW! realise this and they see slipping past them that chance for the Forward to the Middle Ages movement that they so look forward to.

But it's usually only Mondays that I am that cynical.

Tim and ATTP :

Since the radiative forcing models are constant, the common object of " mitigation " is reduced radiative forcing, and it can be reduced by a plenum of means besides carbon policies.

No semantic agression denial , please.

Tim,

I realise that your quote include that policies aren't included (as I think I already mentioned in one of my comments) but I'm still not sure I see how they are explicitly scenarios that require no policies, or that this is what is implied. Saying that they don't consider the policies and saying that no policies are required aren't quite the same. However, that would seem to be a rather trivial issue and not one I particularly want to dispute or not.

My standard position is that every economist who studies this says let’s have a carbon tax. And on insurance grounds at the very least, yeah, OK.

Well, yes, that's why I brought that up.

My own belief, not something I would want to have to prove, and not something that should perhaps inform public policy either, is that we’ve already done enough. From that SRES it’s obvious that if we can decarbonise, to a great extent, the energy generation systems then we’re done. That’s roughly A1T. And if you look at the detailed estimates of energy production that make that up I’d say we’re ahead of schedule there. Because it’s not deployment of, say, solar that matters, it’s getting it cheap enough that people will naturally, preferentially, install it. And we’re just about there, aren’t we?

Problem pretty much solved.

Very optimistic, and I think many disagree. This has gone on long enough, but I'll make a point for you to ponder. Consider the figure in David Roberts's post that you criticised that shows the various modelling scenarios. We're currently emitting 40GtCO2/yr. I see a number of people arguing that the developing world needs coal. It's hard, if that were to occur, to see how global emissions wouldn't then increase. Given where we are now and given a potential increase in global emissions, which emission pathways are actually viable?

Russell,

Since the radiative forcing models are constant, the common object of ” mitigation ” is reduced radiative forcing, and it can be reduced by a plenum of means besides carbon policies.

Yes, I agree that the object is to reduce radiative forcing and that there are alternative mechanisms for doing so (I wasn't arguing for or against carbon policies). Some of the alternatives, though, carry their own risks and some don't address everything (ocean acidification, for example).

Tim,

hey see slipping past them that chance for the Forward to the Middle Ages movement that they so look forward to.

I have to admit that this is quite a telling comment.

"So why is it that everyone hates libertarians?"

Libertarians deny the concept of externality, or assign it to a very minor roll in their thinking.

http://www.investopedia.com/terms/e/externality.asp

[That's a link to a defn of externality, not any evidence that libertarians deny the concept. I think you're wrong -W]

Burning fossil fuels produces only only energy for the burner, but also produces CO2, which accumulates in the atmosphere, changes the climate, eventually doing significant harm to others. All burners of fossil fuel collectively have the responsibility to reduce releases of CO2 to avoid that future and distant harm to others.

A Libertarian will disagree with that statement. Not because the statement is false, but because it doesn't fit into the Libertarian world view.

[Or, because its wrong. The std economic response to externality is to pay for it. Not reduce things causing it -W]

The septic variety of Libertarian will deny that CO2 is accumulating, or that CO2 causes climate change, or that climate change will harm others. The economic Libertarian will deny that anything other than profit should matter to the burner of fossil fuels, as a richer society today will lead to a richer society in the future, offsetting the harm of climate change.

I'm not a believer in infinite growth in any form (See comment #14). I suspect that future societies might not be richer, and might even be poorer than today's society, and that the future harm of climate change will not be offset by accumulated wealth from past burning of fossil fuels.

http://www.cisl.cam.ac.uk/business-action/natural-resource-security/nat…

"The std economic response to externality is to pay for it. Not reduce things causing it -W]"

-- but, pay for it with what? Money? That creates more externalized costs.

Reducing externalizes costs will cut profitability by about a third* --- that part of the money profit is fake.

You can't pay for externalized costs with money that requires continuing to externalize costs.

See anything funny about that? Or the state of the planet?

*http://www.theguardian.com/environment/2010/feb/18/worlds-top-firms-env…

[The context here is the libertarians, wanting "free" environmental damage; or so PH asserts. Within that context, being forced to pay removes the "problem", from an economic viewpoint. And yes, you pay with money, that does things. So if the externality was your plant polluting a water supply, perhaps the money would pay for cleanup or somesuch -W]

http://raikoth.net/libertarian.html#externalities

So you are a weak externality variety of Libertarian, OK. Easier to talk to than the "Taxation is Theft" variety.

So riddle me this, then how does a tax on an action paid today in country A, and spent on concerns of country A shortly thereafter, in any realist way offset or pay for the harm to citizens of country B a half a world away and a hundred or more years later, that are harmed by that taxed action?

[Timmy answers this correctly below -W]

Sure, taxation will cause some reduction in the amount of the action causing harm, I get that. But it seems likely to me that the current generation in mostly wealthy countries is doing vast harm to people in mostly poor countries far in the future, damage that is very likely to be not paid for or compensated for in any way.

"Sure, taxation will cause some reduction in the amount of the action causing harm, I get that. But it seems likely to me that the current generation in mostly wealthy countries is doing vast harm to people in mostly poor countries far in the future, damage that is very likely to be not paid for or compensated for in any way."

The aim isn't to compensate. Nor even to raise revenue. The aim is to change market prices.

It's called an externality for a reason. The damage is not included in market prices. It's thus external to the whole calculation that the market economy does, based upon prices. The sole and only point of bringing in a carbon tax (as an example of such taxes) is to bring the emissions into market prices so that resource allocation is informed by the costs of those emissions.

That's it, that's the whole justification.

You can also have compensation if that's what you want. But the carbon tax isn't there to provide it, not its function at all.

It really does just follw from this: emissions cause damage. That damage is not in market prices. Thus there will be more such emissions than there "should" be, as the benefits of making emissions are not being counterbalanced by the damages that come from emissions. So, add the tax to include the costs of the emissions to market prices. Now, the market, that great calculating engine (really, the only one we've got that can calculate something as complex as a whole economy, see Cosma Shalizi's essay, In Soviet Union Optimisation Problem Soves You) will make sure that emissions only take place when the benefits to the emitter equal or exceed the damages of the emissions.

Note that no one is even pretending that the tax should compensate. Nor that it should halt all emissions, nor all damages caused by emissions to people who are getting none of the benefits. Only that emissions that produce less benefit than the damages they cause will cease as a result of the tax.

We're trying to maximise human utility over time (as, obviously, we always should be). Thus we want emissions that have greater benefits than costs to take place. And we don't want emissions that have fewer benefits than costs to take place. That's what the carbon tax does. And again, it doesn't even pretend to look at the distribution of those benefits and costs: only at the gross amounts of each.

As Ankh said elsewhere

http://www.ginandtacos.com/2008/08/31/atheistsfoxholes-libertariansairp…

"Amid the pie-in-sky libertarianism, free-market circle jerks, and talk of regulation as a criminal enterprise, I suddenly want to be surrounded with libertarians on this plane. I want them as brave volunteers for my experiment in the majesty of the unfettered free market at 35,000 feet. Like there are allegedly no atheists in foxholes, I intend to prove that there are no libertarians in airplanes."

> perhaps the money would pay for cleanup or somesuch

Better air filters, perhaps.

I absolutely hate libertarians.

[Perhaps you are under the illusion that all libertarians are the same. You're welcome to hate Ayn Rand's version, if you like, but assuming that all libertarians are like that is just silly -W]

The whole self interest thing is a real non sequitur.

Now, I need to go to the north forty and construct that 666 story mile high super skyscraper that will raise my agricultural land values from $0.00000001/hectare to $0.00000002/hectare.

Suggest you urban keyboard jockeys go cannibal for the next few years or eat gold and works of art.

How long growth can go on doesn't have much meaning for climate. What should we do differently whether growth is finite or not?

"The std economic response to externality is to pay for it. Not reduce things causing it -W]"

"So if the externality was your plant polluting a water supply, perhaps the money would pay for cleanup or somesuch -W]"

So maybe the best use of the externalities money is to reduce things causing it. If the only way to buy out the externalities is a carbon tax, the proceeds of that tax must reduce carbon fuels use to ensure the money is actually paying for the externalities. Revenue neutrality reduces - I think dooms - the effectiveness of a carbon tax.

The core Libertarian concept is individual liberty. They resist state imposed taxation, but interestingly enough, wholeheartedly support voluntary self taxation. Milton Friedman's son wrote a book about it in the late 70's.

" If the only way to buy out the externalities is a carbon tax, the proceeds of that tax must reduce carbon fuels use to ensure the money is actually paying for the externalities. Revenue neutrality reduces – I think dooms – the effectiveness of a carbon tax."

But the aim isn't to buy out the externalities nor to compensate. It's simply to stop emissions that have lower benefits than the damages they cause. That's all. That's all anyone ever even pretends is the purpose.

"But the aim isn’t to buy out the externalities nor to compensate. It’s simply to stop emissions that have lower benefits than the damages they cause. That’s all. That’s all anyone ever even pretends is the purpose."

That, of course, would be enough, if a considerable part of the pie had not already been baked and sitting in the oven waiting to pop, out including collapse of various ice shelves in the future and more. So no, funding is necessary for reducing atmospheric carbon loading which has already reached dangerous levels.

Oh yeah, GDP fans, take a look at this

http://www.motherjones.com/kevin-drum/2015/05/chinas-future-take-2

> the aim isn’t to buy out the externalities nor to compensate.

There's your problem. It's also called "shifting baselines" -- assuming the damage you live in is the natural world.

A friend of mine refers to the fancy home magazines as "homeowner porn" -- a supernormal stimulus that captivatesm, to render the consumer incapable of being satisfied by what's available in reality.

___________________

“Conservation is getting nowhere because it is incompatible with our Abrahamic concept of land. We abuse land because we regard it as a commodity belonging to us. When we see land as a community to which we belong, we may begin to use it with love and respect.”

“One of the penalties of an ecological education is that one lives alone in a world of wounds. Much of the damage inflicted on land is quite invisible to laymen. An ecologist must either harden his shell and make believe that the consequences of science are none of his business, or he must be the doctor who sees the marks of death in a community that believes itself well and does not want to be told otherwise.”

― Aldo Leopold, A Sand County Almanac

____________________________________________

'ibertarianism is socioeconomic porn. It's not alone in that toxicity -- all the extreme perspectives are comparably blind.

Oh, yeah, and this:

"emissions that produce less benefit than the damages they cause will cease ..."

is that porn in a nutshell. Cleave to it, it's better than reality.

I'm late with this, but Noah Smith, a physicist turned economist, was not impressed with Murphy:

http://noahpinionblog.blogspot.com/2012/11/murphys-law.html

[Thanks. That makes one of my points rather strongly: that the "economist" in the dialogue seems rather fake and deeply ignorant and probably imaginary. Indeed, quite possibly the sort of economist that a physicist might invent :-) -W]

I don't know what you are not seeing. It's a simple argument.

If necessities cannot grow without bound and the economy grows without bound, the delivery of necessities becomes an infinitesimal part of the economy. But unlike 'decoupled" luxuries (movies, education, sport), whose supply is essentially unlimited, by hypothesis the coupled necessities (food, energy) are limited.

If we are both hungry and you have a little food there is no number of tickets to Avengers: Age of Ultron I have to offer you.

It is really hard to fathom how an economy, in which scarce goods have infinitesimal cost and unlimited goods have high cost, could possibly work.

[Ah, I see. But who says food will be scarce? There's plenty of it at the moment; will that change? -W]

The business about cornering the market is just an attempt to think about what would actually happen in this event. It's a sideshow. So far none of the answers I have seen really address the point.

Reagrding noahpinion's (Noah Smith's) piece, again, this basic mathematical point is avoided. Instead we begin with a "no true Scotsman" argument that holds no water.

"The "long term trend growth" that is used in growth and business cycle models is only meant to represent a trend that lasts longer than the business cycle - so, longer than a decade or two."

OK, leaving aside this bit of important counter-evidence, Noah Smith says "Do economists' models crucially hinge on the idea that economic growth will continue forever and ever and ever? No."

Well, cool. So there is no such thing as IPCC WG III.

So this fellow seems never to have looked at a WGIII IAM, but supposing we grant that five or ten business cycles is more like one business cycles than an infinite number of them. Then we have reached agreement, so I don't understand the problem.

Do we agree, then, that economic growth will end eventually? If so, we can get down to the more fruitful point of arguing WHEN.

[I'm not sure we do; but I'm pretty sure that arguing about exactly when isn't interesting. The end of all growth is likely more than 100 years away -W]

To a mathematician, often a problem of setting a bound begins by proving a bound exists. Murphy claims to have shown that a bound exists. Smith's first objection seems to be that nobody ever claimed that no such bound exists, so the conversation didn't happen.

[Murphy's claim to have found a bound is, IMHO, wrong. Its clearly untested - no worthwhile opponent has attacked it and failed; I think its wrong and so does Noah Smith's; I've pointed out flaws in it which you haven't addressed -W]

Then he turns around and suggests that the bound doesn;t exist!

That is. Smith suggests (with a surprising insouciance about the relationship between computation and entropy, not to mention the whole fraught issue of sentience) that we can have after all unlimited economic growth by uploading ourselves into the Matrix. Thereby, it seems to me, directly contradicting his first point.

So which is it - our plan to upload ourselves into software renditions will save us from the limits to growth? (After you, by all means.)

[No, I don't think that's the solution -W]

Or is it that there are no limits after all because science fiction? Look in the Matrix world there is no limit to anything and GDP is not just unbounded but meaningless. Is this supposed to convince me of anything important?

I think finding Smith more compelling than Murphy in this exchange is surprising.

[I don't think anyone is claiming to have proved that there are no limits; i.e. to have proved that infinite growth is possible; the claim is more limited, that the standard disproofs of this (such as Murphy's) make basic errors -W]

Is that the key? Economics defines away external costs, so any damage that happens outside the "market" isn't real?

[Nooooo... how can you get this so badly wrong? You don't like economics, or what it tells you, I think that's so. But that doesn't mean you need to misunderstand it. How can you fight something you don't understand? There's a nice wikipedia article at en.wikipedia.org/wiki/Externality and it even has a section on "Possible_solutions" -W]

That would explain the diminishing market value of agricultural land - it's been stripmined of living soil and minerals, that value flushed away. What's left isn't worth much without pouring on fertilizer and herbicide, eh?

[Err, no. The market value of agricultural land has been going *up*. Its only been going down as a proportion of GDP -W]

If so it's time to get rid of the blinkered blind market and do our trading as parts of an ecology rather than a marketplace.

The advantage of interacting in an ecology is, it's real.

The disadvantage? Harder to cheat in reality.

"Economics defines away external costs, so any damage that happens outside the “market” isn’t real?"

Blimey, wrong end of stick or what?

Economics recognises that market don't recognise externalities. Economics thus comes up with a solution for this.

This is then described as "economics" defines away external costs?

That wrong end of the stick is big with this one.

> Economics thus comes up with a solution for this.

If anyone wanted a solution, the people to ask are the epidemiologists. They'd have been telling you for years, decades, or more where the costs were going off the table.

That's what I have found so disappointing -- the claimed solution "economics" comes up with, which includes generations of delay accepting any evidence there's a problem, then further delay implementing any solution, while the profit accumulates. And lo, there's enough cash in the spare change drawer to pay the penalties, ow-my-wrist.

[You're doing the same thing that so many others do: failing to discriminate between politics and economics -W]

How much do businesses have to pay to get such compliant politicians? I'm sure there's a good answer.

Oh, I know, I know, theoreticaly, given the rules economics plays by, what economics offers is "not a solution that has failed, but a solution that has never been tried"

Seriously, how does this history differ from the history we're living through now with current 'externalized cost' issues?

It's worth actually reading, and giving a few days' thought and checking some references, if you've not taken any classes in the area.

http://ajph.aphapublications.org/doi/abs/10.2105/AJPH.79.12.1668

W:

OK, but anyone can claim to be a libertarian. How do we tell who is and who isn't one?

[Sorry guv, its the same as with anything: you're obliged to think, not just believe people's claims -W]

> You’re doing the same thing that so many others do: failing to discriminate between politics and economics -W

You're doing the same thing that so many others do; failing to recognize that the allocation of goods is and has always been a consequence of politics.

[No, I'm not. I'm fully aware of that. But its irrelevant to the point, that GDP growth can in theory be decoupled from resource growth -W]

The market as economists currently understand it is a cultural artifact, a single instance of a vast range of possible structures to organize allocations.

Or really only part of the structure, which is the real flaw.

William's shrug ("oh the end of growth is at least 100 years in the future") is symptomatic of this selective blindness. What do we do with the part of our intentions that wants to leave the world workable in two centuries or even three?

[You're back to politics: how do you convince other people that your spiffy vision is better than their short sighted vision? But don't mix that up with confusions like Tom Murphy, who didn't even understand how GDP growth is defined. And you read his stuff. and didn't notice, or care -W]

It may be apocryphal, this story of native tribes in the Americas having a voice for the seventh generation in their councils. But it is at least interesting and plausible.

To limit all resource allocations to a market is to give effectively no voice to the seventh generation. Yet our powers have become immensely greater, and our responsibilities consequently now stretch to something like the seventieth generation.

Dismissing what happens after a century is the problem, not the solution.

> how do you convince other people that your spiffy

> vision is better than their short sighted vision?

Hm. Tom Paine and Ben Franklin talked theirs up rather convincingly on PR trips in England and France, as I recall.

The new vision is convincing to the extent the current one is becoming intolerable. The key is it's not the people who benefit from the old vision who have to be convinced. It's the people with the pitchforks.

http://www.nytimes.com/2013/04/02/world/asia/air-pollution-linked-to-1-…

#45: then so you disagree with this statement: "The std economic response to externality is to pay for it. Not reduce things causing it", for the carbon tax is only in place to reduce the release of carbon, not to pay for the damage?

[Sorry, I was imprecise; Timmy is correct. The purpose is to correct the market prices; "pay" in that sense. "the carbon tax is only in place to reduce the release of carbon" is wrong though: the purpose is as Timmy says and I'm now echoing: to correct the markey price so it includes externalities. Not, directly, to reduce the release of carbon. Though of course it would -W]

If the price is set correctly a carbon tax might well be the best political/economic method of reducing future harm. Ah, but what if the price is set incorrectly? Looks to me like setting a price for carbon involves an economic and technical forecast for the future. That seems a little difficult, to say the least.

[Indeed. But so does anything else. If you cap-n-trade or whatevs, then you need to set the cap, based on some kind of forecast, which might be wrong -W]

"Ah, but what if the price is set incorrectly? Looks to me like setting a price for carbon involves an economic and technical forecast for the future. That seems a little difficult, to say the least."

Yah. "Because prediction, especially about the future, is difficult"...Nils Bohr.

W, in response to my question "OK, but anyone can claim to be a libertarian. How do we tell who is and who isn’t one?":

Snerk - don't be thick. I was trying to pin you down on what you think a person may opine and still be allowed to call himself a libertarian. You told Phil Hays "assuming that all libertarians are like that is just silly", as if only you could draw a circle around the set of all libertarians. If you claim to own the word, can't you tell us what it means?

[I don't claim to own the word. I was responding to EFS, not PH. EFSs claim was "I absolutely hate libertarians" which I thought was silly, as it appeared to think all libertarians the same. My point is that they aren't; they encompass a wide spread from the wide-eyed Randian types to people who just call themselves such but aren't really. As for a defn, the lede of the wiki article seems reasonable to me -W]

> failing to discriminate between politics and economics -W

Well, I'd say economics-and-politics is the group that fails to aggressively identify and manage 'externalized' costs, and does so wilfully and as long as possible.

[That makes no sense; you're still deliberately mixing up econ and pol, to your own confusion. There's piles of econ work on externalities; you've read none of it, but that doesn't mean it doesn't exist. You're talking like the Watties: "climate science? Nah, I call is climate-so-called-science-and-politics, they're mixed up together I tell yah". The Watties are wrong, too -W]

That's the problem I see the ecologists and public health pointing out -- that externalizing costs as a successful business method requires believing they can "go away" -- as

Kim Robinson pointed out, that kind of economics is not a dismal science, it's a cheerful religion.

http://www.env-econ.net/2015/05/a-libertarian-financial-market-analogy-…

[Interesting, if you follow it to the source at https://www.vox.com/2015/5/12/8588273/the-arguments-that-convinced-this….

Note that some of that is just weird, like "Libertarians tend to compare the cost side of climate change [mitigation] to the benefits. They say, when [person or company] A harms [person or company] B, if the gains to A are greater than the harms to B, then fare thee well. No! If you believe in property rights and individual liberty, it simply does not matter if aggression from A gains more than is lost by the victim. I just never thought of it that way. And I thought he was exactly right. So that was the first thing that changed for me."

But we can lay that aside.

"And we know it’s a low-probability, high-impact risk" is an odd way to describe things. It appears to discount all the certain-to-moderate probability risks, that the std analysis relies on. mt (correctly, in my view) frequently points out that low-prob high-impact risks are under emphasised; but I don't think even he would assert that *all* the risk, or even the majority of it, comes from this.

However, the arguments for hedging risk, and the useful analogy with the markets - that people are happy to pay to hedge risk, even low-probability risk - should play well with that sort of person. Note also that support is conditional on the cost being hedging-type cost; not high-cost change-your-lifestyle type costs -W]

Setting a cap or a tax for carbon are political acts.

I'm in favor of a carbon tax, not because it is any better (not clear to me that it is), or that the price can be set more accurately than the cap, but because it seems to be more politically possible. Do note that what the money raised by the tax is spent on, will matter just as much in politics if not more, as the tax itself. If you could manage to replace a tax funding an activity of government (schools, health care, etc.), the tax rate would be more influenced by the amount of money needed for that activity than by the actual correct price for carbon, assuming it could be determined with any accuracy.

[For some of my earlier reflections, arguing for a tax not cap, see Carbon tax now -W]

So, Tim, Tom,

Am I fundamentally missing something here? It seems that Tom's argument concerns ENERGY, and the data show that the ENERGY we use increases with GDP,

[Notice you've provided no citation for that. And notice that in principle there's no reason why energy use has to go in step with GDP. And notice that in recent years, indeed, it hasn't. See for example http://data.worldbank.org/indicator/EG.GDP.PUSE.KO.PP.KD/countries?disp… which shows that GDP per unit of oil has gone up from 6.7 in 2005 to 7.3 in 2011 -W]

however you want to measure GDP (by the way, reading and re-reading Tim's comments and blog, it seems that economists just....well....make stuff up — not lie, but rather, hey, lets just add some digits to these numbers because it's something we can't really define but we'll call it "value"). So, I can't see anything that Tim says that counters what Tom says. But, Tim's a clever guy, so I must be missing something. So what is it?

http://dx.doi.org/10.1016/j.jaridenv.2014.01.016

"... Zero Net Land Degradation (ZNLD) policy. The concept of ZNLD proposes a scheme under which the extent of global degraded lands will decrease or at least, remain stable. To enable this type of scenario, the rate of global land degradation should not exceed that of land restoration. Restoration efforts should include not only croplands, rangelands, and woodlands, but also natural and semi-natural lands that do not generate direct economic revenues. The United Nations Convention to Combat Desertification (UNCCD) envisages achieving this target by 2030. Despite being seemingly ambitious, the target of ZNLD could be achieved if degraded lands are restored to a considerable extent and, at the same time, land-degrading management practices are replaced with ones that conserve soils...."

Achieving Zero Net Land Degradation: Challenges and opportunities

Journal of Arid Environments

Volume 112, Part A, January 2015, Pages 44–51

Special Issue on the Fourth Drylands Deserts and Desertification “DDD” Conference

Well, I thought I work my way through this 'infinite' thread.

So 1st up the 'infinity' assumption, is that the same as the 'beyond infinity' assumption?

The thought of someone even saying infinite growth is rather mind boggling to say the least.

It's like me saying, look at me, I have infinite wealth, the next person says, well that isn't nothing as I have 2X your infinite wealth. (per year mind you, as in last year I had infinite wealth, this year I have 2X infinite wealth, next year I'll have 4X infinite wealth, as infinitum, ad nauseam).

So the question becomes just how many infinities are there to infinite growth? Infinity. D'oh!

[But consider salt: the annual economic salt activity is probably low enough that Bill Gates could buy it all. But (a) why would he bother, and (b) if he tried to corner the market, the price would go up -W]

Very interesting hypothetical (as the verklempt Curry would say)..

It's like me saying I cornered the sand market. It's not like there isn't a whole bunch of sand, err, salt in the oceans. Or iron, yeah, that's the ticket, I've cornered the iron market. Even better, I've cornered the tree market, cut them all down, have all the seeds, I"m the tree Nazi, no trees for you.

Finally, I thought Darwin had something to say about unbound species growth. Oh wait, that's not economics, as economics is purely a human construct, cue Imaginationland.

.

So someone gave me the Mona Lisa painting (trust me I have the real thing, you all will just have to watch the next Tom Hanks movie due out in 2016).

Anyways, got a gas can, touched the damn thing, Timmy was there, so he and a whole bunch of other people saw me do it.

There I was thinking, see no value in ashes are there?

But, n-o-o-o-o-o-o-o-o-o-o-s, people saw value in those ashes, because it use to be the Mona Lisa painting.

Long story short? Timmy bought those ashes for like a jillion dollars, w-a-a-a-a-a-a-a-a-a-a-y more than I could have ever have gotten with the original Mona Lisa painting.

Moral of the story? Value.

> hedging-type cost; not high-cost change-your-lifestyle

> type costs -W]

Hedging drastically limits most people's possible lifestyle:

-- maintaining a standing army and an educated populace is hedging, for example. Odds are you don't need it personally, but someone might. Health insurance; vaccination; sanitation -- heck, most civilization is hedging against 'ibertarianism, no?

[The army (or the nooks) is indeed a useful example of hedging; although I think if you pushed that example at the right wing they would tell you that the army actually provided a deterrent function, so isn't pure hedging. Education isn't hedging, nor sanitation: they are both clearly useful in themselves -W]

Not really.

On infinite growth, two things to remember.

1) there's no such thing as a free lunch (even if it's free for you), and

2) water doesn't flow uphill by itself. Or, if you prefer the nihilist version, all bleeding stops (yeah, that one reqires homework...).

Of course if you ignore these two points you can imagine infinite growth (though getting the universe to listen to you might be somewhat harder than the imagining) and, curiously, you can draw a god-shaped space (though whether you can fill it or not depends again, ironically, on what the the universe has in mind...)

A handy rule for the executive summary is that, entropy aside, there's no physical basis for infinite growth of anything* within the universe.

[We're not talking about physical growth -W]

You can hide under your pillow but it doesn't change this fact, and the best that you can hope for is to optimise the arrangement of the daisies in your own corner. And that you do not forget that the garden is what feeds you, you little agent of entropy, you...

[*The jury seems to be out when it comes to expansion of the universe, and for giggles at the pub it's entertaining to ponder whether this might have something to do with aforementioned entropy - I've said in the past that it would be an interesting quirk if there was no actual dark energy, other than an entropy 'engine' blowing up the balloon... Is it a corollary of conformation to the Second (and First) Law?]

William,

Timmy has a post:

http://blogs.telegraph.co.uk/finance/timworstall/100017248/infinite-gro…

If you and Timmy can derive a sort of asthmatically, err (spell checker knows better than I), mathematical proof, WITHOUT invoking 'advancing technology' Alfred has a special prize waiting for you too, err, two.

The Neuman Memorial Prize in Economic Sciences

That prize predates that other 'prize' by oh say 14 years.

Jeebus, talk about missing the point:

"WITHOUT invoking ‘advancing technology’"

We all agree that there's a bound, a limit, to the resources that can be used. We're also stating that the limit to economic growth is the ability to add value. As a result of advancing technology.

So, obviously, if we can't call ino being the ability to add more value, as a result of advancing technology, then the bound to economic growth is resource availability.

We already agree all of that.

So marching in and declaring that, well, we're talking about advancing tech is, well, it's proper AE Neumann, isn't it? Because, umm, yes, we are.

So, a small test. 30 years ago, connector fingers on computer boards used 200 nm gold plating. Today more like 2 nm. So, from the same amount of gold, from that same limited resource, can we add more value through advancing tech?

I say yes, you say what?

Err,

See post #72 above please? Address that one 1st if you don't mind.

[There's nothing to address there -W]

I'm not the one who brought infinity into this or any other discussion that I am aware of. Until that's addressed it's kind of pointless to continue (Planck time/lengths notwithstanding,if you know what I mean).

So there I was thinking I could get to light speed

[You can't. Physical constraints intervene. You don't appear to have understood yet that the same doesn't apply to economics -W]

and that there was this place with a 'perfect' vacuum. And that if I could only go below absolute zero in that 'perfect' vacuum there would be no light pressure, but alas, the universe is not truly 'empty' and thus I will forever be chasing the speed of light, or is it running into the speed of light. Lots of photons out there don't'ca know?

You do know that Earth is the center of the (observable) universe? Geocentrism! (well sort of, not the generally accepted definition, but well, it works for me)

Oh, excuse me, I went of on a tangent there, back to reality.

Infinity. Other than, number divided by zero, in quad precision Fortran is NaN, what was it you were saying about infinity again?

So William, let's do some dimensional analysis, with this thing you call economics, shall we.