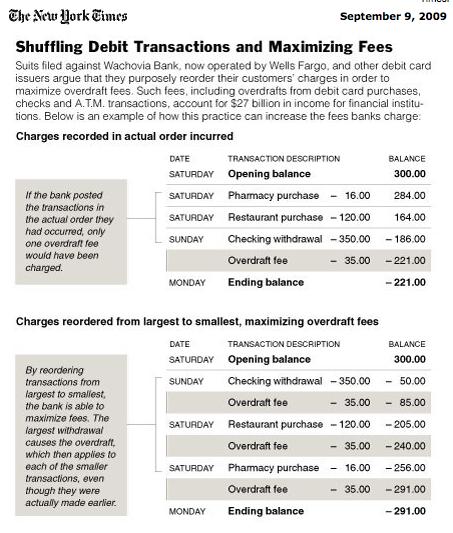

...you should go out of business. I've meant to get to this, so in Internet years, this news is like a gajillion years ago. Anyway, one of the galling things about the bank bailout is that, even though in many cases the taxpayers basically own the banks, nothing is being done about various forms of usury, one which is banks' effort to maximize overdraft fees. Here's an example of what I mean:

Naturally, banks are trying to push back:

Some experts warn that a sharp reduction in overdraft fees could put weakened financial institutions out of business.

Michael Moebs, an economist who advises banks and credit unions, said Ms. Maloney's legislation would effectively kill overdraft services, causing an estimated 1,000 banks and 2,000 credit unions to fold within two years. That is because 45 percent of the nation's banks and credit unions collect more from overdraft services than they make in profits, he said.

"Will they be able to replace it with another fee?" Mr. Moebs said. "Not immediately and not soon enough."

They will certainly try. For instance, some banks have said they might slap a monthly fee of between $10 to $20 on every free checking account. At the moment, people who pay overdraft fees help subsidize the free accounts of those who do not.

I call bullshit. There was a time, admittedly so long ago that liberals freely roamed the political landscape, when banks made profits and didn't have to have to gouge customers. In fact, they made profits, and debit cards hadn't even been invented yet (terrifying, isn't it, kids?). How did they do this?

Well, their loan portfolios didn't suck ass. If a bank is making more money by essentially offering payday loans (via overcharge fees) than they are by loaning money that they receive from the Fed at very little cost*, then they should go out of business. FDIC will backstop the deposits, and the good loans will be acquired by healthy banks.

AAAIEEEE!!! TEH SOCIALISMZ!!!

*The rest of us would be so lucky to get those rates.

I've never understood the appeal of debit cards. I view a purchase card tied directly to a bank account as a security risk. Yeah, yeah, I know: there is a lot of wordage saying the bank protects against theft much the same as with a credit card. Maybe so. But with a credit card, the money is never gone from my account. And while I've never had a dispute with a bank over a card charge, my intuition is that it is far, far easier not to pay a disputed charge than it is to get a refund for a charge already taken from one's account.

I don't understand people who use cheques and cash instead of debit cards. I've been using one for well over a decade and have never had an issue (mind you I don't write my PIN on the back like some people).

OTOH I have had to dispute charges on a credit card (AMEX) and the mediation process was painful.

My roommate had that exact gouge done to him. The bank put the withdrawals before the deposits(despite it not being correct chronologically), and he ended up overdrafting with over $100 in fees. He tried to fight the bank on it, but only got 50% back

Has nobody noticed that a lot of the latest account management "features" and procedures seem to be designed to maximize the chance that you'll screw up?

"You get free checking if you let us move $50 a month from your checking account to your savings account," and, "We're helping you save by rounding up your debit card purchases and moving some of your coinage from checking to savings," both really translate into, "We want to minimize the likelihood that you know your exact balance and maximize the chance that you'll overdraft."

Who actually thinks that "Keep the Change" from BofA actually makes *any* sense to for the customer? Does, "We arbitrarily scoot trivial amounts of your money from one place to another," really appeal to anybody?

Back in the day, I bought some goods online with a debit card - and the company went bankrupt. I was reimbursed about 10% of the total, people who used credit cards were reimbursed 100% (amongst my group of friends, that is).

So credit cards make more sense, and they can't do this sort of BS (obviously late fees are a whole 'nother deal, but most people generally know about those).

I call BS on Moebs' excuse as well. Sound like the words of a dying company that's desperately trying to rape their customers wherever possible, no matter how outrageous.

This isn't anything new; banks have been playing this scam for years. What's changed is that this is now, for too many banks, the difference between green ink and red ink in the quarterly earnings statements. Also, with debit cards becoming increasingly prevalent, more people are running into this scam (back in the old days, it was just checks, not debit card sales). Good on Ms. Maloney for introducing legislation to stop the practice.

Shuffling charging like that should be criminal.

On another note. I have never had a debit card and I never will. I do not consider them safe at all. I use a credit card and I pay the balance in full every month. I have never paid interest and have been using credit cards since the early 1970s.

Actually banks pay ME. I get double credit some places.

For me the main issue isn't necessarily the fact of overdraft charges but the quantity and magnitude. Being charged a $35 overdraft on a couple-of-hundred dollar bill payment is an annoyance; being charged five $35 fees on five charges of less than ten dollars when you don't realize you're overdrawn in the first place is downright insipid.

I would argue that overdraft charges should be based on the size of the transaction made. It shouldn't matter to BoA whether I'm a hundred dollars in the red based on one big payment or several smaller ones -- either way, they're on the hook for the same amount.

I'd like to add that I've seen many cases where the overdraft was not actually paid, but the fee was charged. That doesn't really make sense in light of the claim that overdraft fees are fees for the "service" of not denying your request for money. It costs them basically no money to decline a charge, and it's very hard to argue that declining a charge is a service in any meaningful sense.

The Australian government has just introduced legislation aimed at eradicating those types of charges which are clearly a form of fraud.

Used to be that accounts were updated after the banks closed and the rule was that all deposits were entered before any withdrawals. I was under the impression that banks' account5ing systems had to emulate this. Clearly in the case shown here they aren't doing that.

"which are clearly a form of fraud."

BINGO... if you or I somehow ran this scam on people we would go to JAIL. But of course, for this, nobody will (they'll get productivity bonuses instead).

I have no idea why people think that credit cards are better than debit cards. You pay interest on credit, you don't pay interest if you don't use credit.

As a contract worker, I found out young what happens if you lose your income and are as little as a couple hundred bucks in the hole. Consumer and revolving credit are tools of the devil.

Anyone who can pay off a credit card regularly can keep themselves a few thousand ahead of the game, and not risk becoming an indentured servant. All you have to do is decide what level you are comfortable with, and use the same techniques you have already been using to keep yourself no more than $5000 down. Just adjust your thermostat.

I have no idea why people think that credit cards are better than debit cards. You pay interest on credit, you don't pay interest if you don't use credit.

1. As BankruptElf noted, when you buy something with a credit card and the merchant goes bankrupt before they can ship your order, you're protected. With debit cards, they already have your money, and you are therefore an unsecured creditor.

2. Most credit cards (at least every one I have ever had) come with a grace period: if you pay the entire balance by the due date, they don't charge interest on your purchases. Primarily a benefit to people like me who pay off the balance every month. Conversely, if you happen to be short on cash that month but it's a temporary condition, you don't have to pay the full balance--with debit cards you always do, and you run the risk of depleting the bank account. Also, with credit cards you have some control over timing (i.e., you can wait until after your paycheck is deposited to pay the bill), but with debit cards the charge hits your bank account no later than the next business day.

3. If somebody steals your debit card number, he can deplete your bank account with relative ease. If somebody steals your credit card number, it's a lot harder, as the credit card company must eat the loss on anything over $50.

4. There are still some things you can do with a credit card that you can't easily do with a debit card. For instance, most rental car companies won't let you rent a vehicle with a debit card.

The one downside of credit cards is that it's easy for somebody with no financial discipline or some serious bad luck to get in way over his head, mainly because of the interest charges. But debit cards are not adequate protection against this either: the overdraft charges are a backdoor way of charging interest at rates that credit card companies can only drool over.

At most financial institutions, the wording actually says that credit-card like protection only applies to transactions reported within 2 business days of the transaction. That's a great deal less protection, even in the best of circumstances.

Used to be that accounts were updated after the banks closed and the rule was that all deposits were entered before any withdrawals. I was under the impression that banks' account5ing systems had to emulate this. Clearly in the case shown here they aren't doing that.