...if by stimulate, you mean wind up in banks that aren't lending any money. From the Bureau of Labor Statistics:

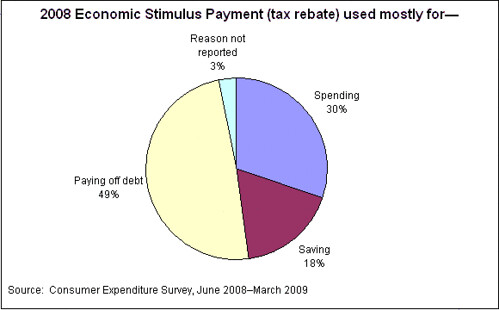

In May 2008, the Internal Revenue Service (IRS) started mailing Economic Stimulus Payments (also called tax rebates) to an estimated 130 million income tax filers. In order to examine the impact of these payments, special questions were included in the Interview component of the Consumer Expenditure Survey from June 2008 through March 2009 to collect information on the amount of payment received, form in which it was received (electronic funds transfer or check), and how it was used (mostly for spending, saving, or paying off debt). This report contains the first analysis of these data.

So, nu, what did they find?

That's right: two-thirds of the money either went to pay off debt or sit in bank accounts. Now, that's not an entirely bad thing, unless banks aren't loaning money--which is what they're doing right now. This is why I typically don't favor tax cuts as a way to stimulate the economy, as opposed to government spending. Money has velocity*: the more times a particular dollar is spent (i.e., the number of hands it passes through), the more jobs are created. Giving people a hunk of money, which then gets parked in a non-lending bank one way or another, isn't the best way to put people back to work. In fact, Compulsive Contrarian Disorder victims notwithstanding, the best way to get unemployed people back to work is to hire a bunch of people to do stuff.

TEH SOCIALISMZ!!! AAAAIIIEEEE!!

*I'm just a Mad Biologist. I'll let the economists and physicists duke it out over who is misusing this term.

Economists are like poets. They're not misusing the term "velocity", just borrowing it for a metaphor.

I'm telling you this so that when they start in about the "DNA of money"* you don't get upset.

*Future metaphor alert.

Mike, you are being unrealistic. I don't see how you can expect banks to lend out that money when they need it all to pay bonuses to their executives.

This is yet another instance of individual players taking steps which are rational for them personally but not for the economy as a whole.

We're in a deflationary environment for now, so cash is king and debt is bad. So most instances of people using their tax rebate to either pay down debt or increase savings are rational.

There are also some banks for whom not lending more money is the correct thing to do, although other banks which aren't lending money should be. With increased risk of default, or increased actual defaults, many banks really should be increasing their reserves, and the easiest way to do this is by taking in deposits (or accelerated debt repayments) which don't get turned into loans. It sucks for the economy as a whole that these banks aren't lending, but there are some banks who really shouldn't be lending.

As for "velocity of money": It's a metaphor, but a perfectly reasonable one. (Strictly speaking, it should be "speed" rather than "velocity"--it's a scalar, not a vector--but that's a minor point.) It measures the rate at which a particular unit of currency changes hands. The number of transactions involving a particular currency unit is a reasonable stand-in for distance, and distance divided by time is a velocity. (For the record, I'm a physics type.)

DNA of money, you say?

http://www.google.com/search?q=%22dna+of+money%22